The end of the liquidity driven rally. What lies ahead?

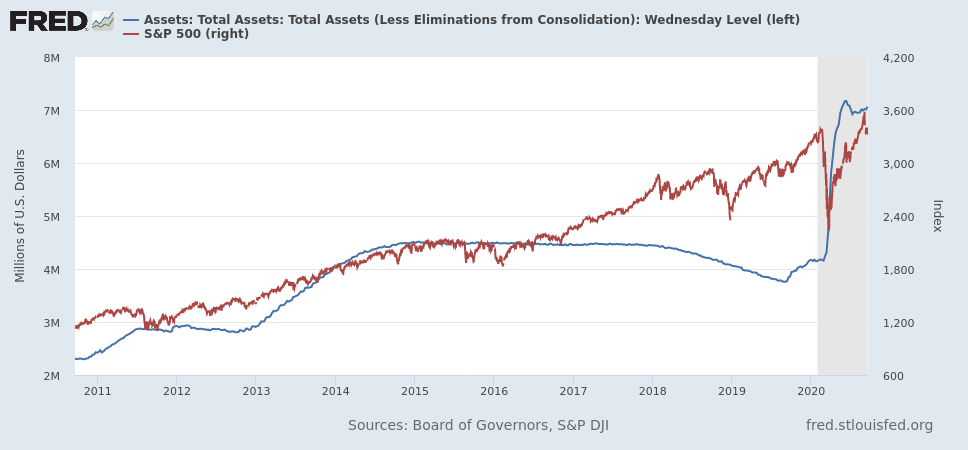

The economic crisis which sparked from the global pandemic created the perfect storm for ‘money printing’ by the Fed. The liquidity response to the crisis was very strong, highlighted by the direct purchases of corporate bonds and stock market ETFs for the first time in Fed’s history. However, the vast majority of the liquidity came through monetization of debt processes as the Fed purchased trillions of Treasuries and government bonds turning debt into liquidity for the markets.

Low interest rates and increased liquidity are a direct consequence of the Fed cutting interest rates and expanding its asset purchase policy to include corporate and municipal bonds. Liquidity and low real yields have been the primary drivers of the S&P 500’s rally from the March 23 bottom but the liquidity driven market rally now seems to come to and end as shown in the graph below.

It is unclear if and how the Fed will eventually respond to the end of this rally. The Fed avoided adding to QE on Wednesday which caused the markets to lose some more momentum. This may be deliberate to keep some powder dry ahead of pressures for even cheaper money in the months ahead.

It is obvious that another liquidity boost will keep moving markets but even if the Fed unleashes liquidity bazookas again it would be like further blowing a bubble. Drifting investments away from the real economy and inflating valuations of financial assets may not be constructive or inflation-inductive.

Our view is that investors should remain cautious going forward.